Home Sales Were Steady in August After Four Straight Months of Decline.

Existing-Home Sales Decline Across the Country in September

Existing-home sales remained steady in August after four straight months of decline, according to the National Association of Realtors®.

Existing-home sales declined in September after a month of stagnation in August, according to the National Association of Realtors®. All four major regions saw no gain in sales activity last month.

Total existing-home sales1, https://www.nar.realtor/existing-home-sales, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, fell 3.4 percent from August to a seasonally adjusted rate of 5.15 million in September. Sales are now down 4.1 percent from a year ago (5.37 million in September 2017).

Lawrence Yun, NAR chief economist, says rising interest rates have led to a decline in sales across all regions of the country. “This is the lowest existing home sales level since November 2015,” he said. “A decade’s high mortgage rates are preventing consumers from making quick decisions on home purchases. All the while, affordable home listings remain low, continuing to spur underperforming sales activity across the country.”

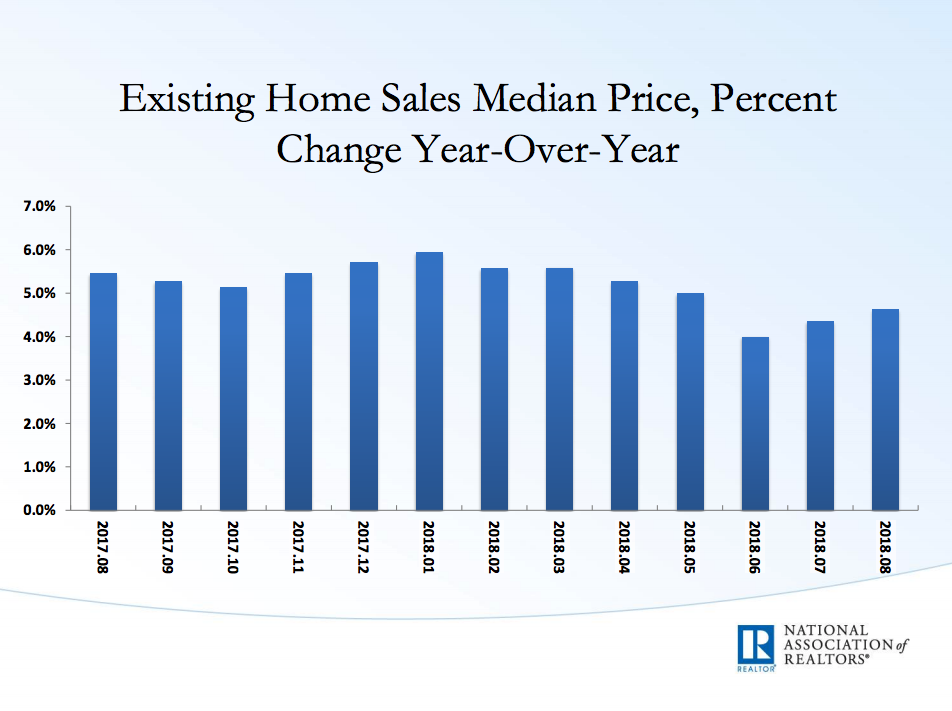

The median existing-home price2 for all housing types in September was $258,100, up 4.2 percent from September 2017 ($247,600). September’s price increase marks the 79th straight month of year-over-year gains.

Total housing inventory3 at the end of September decreased from 1.91 million in August to 1.88 million existing homes available for sale, and is up from 1.86 million a year ago. Unsold inventory is at a 4.4-month supply at the current sales pace, up from 4.3 last month and 4.2 months a year ago.

Properties typically stayed on the market for 32 days in September, up from 29 days in August but down from 34 days a year ago. Forty-seven percent of homes sold in September were on the market for less than a month.

“There is a clear shift in the market with another month of rising inventory on a year over year basis, though seasonal factors are leading to a third straight month of declining inventory,” said Yun. “Homes will take a bit longer to sell compared to the super-heated fast pace seen earlier this year.”

Realtor.com®’s Market Hotness Index, measuring time-on-the-market data and listings views per property, revealed that the hottest metro areas in September were Midland, Texas; Fort Wayne, Ind.; Odessa, Texas; Boston-Cambridge-Newton, Mass.; and Columbus, Ohio.

According to Freddie Mac, the average commitment rate(link is external) for a 30-year, conventional, fixed-rate mortgage increased to 4.63 percent in September from 4.55 percent in August. The average commitment rate for all of 2017 was 3.99 percent.

“Rising interests rates coupled with increasing home prices are keeping first-time buyers out of the market, but consistent job gains could allow more Americans to enter the market with a steady and measurable rise in inventory,” says Yun.

First-time buyers were responsible for 32 percent of sales in September, up from last month (31 percent) and a year ago (29 percent). NAR’s 2017 Profile of Home Buyers and Sellers – released in late 20174 – revealed that the annual share of first-time buyers was 34 percent.

“Despite small month over month increases, the share of first-time buyers in the market continues to underwhelm because there are simply not enough listings in their price range,” said NAR President Elizabeth Mendenhall, a sixth-generation Realtor® from Columbia, Missouri and CEO of RE/MAX Boone Realty. “Entry-level homes remain highly sought after, as prospective buyers are advised to contact a Realtor® as early in the buying process as possible in order to ensure buyers can act fast on listings that catch their eye.”

All-cash sales accounted for 21 percent of transactions in September, up from August and a year ago (both 20 percent). Individual investors, who account for many cash sales, purchased 13 percent of homes in September, unchanged from August and down from 15 percent a year ago.

Distressed sales5 – foreclosures and short sales – were 3 percent of sales in September (the lowest since NAR began tracking in October 2008), unchanged from last month and down from 4 percent a year ago. Two percent of September sales were foreclosures and 1 percent were short sales.

Article and data provided by the National Association of Realtors (NAR) 2018

{kind=link}